The Current “Digital Closing” is a Lie

The industry sells a story about digital transformation in real estate closings. This story is mostly fiction. What we have today is not automation. It is a fragile layer of web forms and e-signature APIs plastered over a seventy-year-old process. We swapped manila folders for PDFs and convinced ourselves we innovated. The core logic, the sequential human approvals, and the institutional delays remain untouched. The system still runs on email and phone calls.

We are just pushing digital paper faster. The bottlenecks are the same. A title agent still manually pores over a chain of title. An underwriter still logic-checks loan conditions based on documents scanned at different DPIs. A county clerk still waits for a batch file to update a mainframe. The entire Rube Goldberg machine of faxes, wires, and “wet signatures” was simply given a prettier user interface.

This is not a scalable architecture. It’s a liability held together by overworked paralegals and institutional inertia.

Architecting for State Change, Not Document Flow

A real estate transaction is fundamentally a state change. Ownership of an asset, identified by a legal description and parcel ID, is transferred from Party A to Party B, conditional on the fulfillment of contractual obligations. The current process buries this simple state change under a mountain of documentary evidence. We generate hundreds of pages to prove the transfer happened, instead of focusing on executing the transfer itself as a single, atomic operation.

A forward-looking architecture must treat the property title as a programmable object, not a historical narrative in a dusty county ledger. The goal is to build a system where the transaction’s execution and its recording are the same event. We need to gut the distinction between signing a document and finalizing the transfer. The signature should BE the transfer.

This requires a complete teardown of the existing workflow. You cannot bolt this concept onto a title company’s existing software stack. You have to re-platform the entire concept of a title record, moving it from a database of scanned images to a distributed ledger where the asset itself lives as a unique, non-fungible token.

Forget the cryptocurrency hype. Think of the ledger purely as an engineering tool: an immutable, auditable, and programmatically accessible database for high-value assets. Its primary function is to eliminate the need for reconcilers and insurers who exist only because traditional databases are centralized, mutable, and opaque.

The Tokenized Title: A Data Structure

The first step is to represent the asset in a structured, machine-readable format. Instead of a 50-page title report, you have a JSON object representing the asset’s current state. This object contains every critical piece of data needed to validate and execute a transfer. It is the single source of truth, cryptographically secured and historically verifiable.

A simplified version of such a data structure might look something like this:

{

"property_token_id": "0xABC123...",

"parcel_id": "04-16-300-021",

"legal_description": "LOT 42 IN BLOCK 11 IN...",

"owner_public_key": "0x987DEF...",

"status": "ACTIVE_LISTING",

"liens": [

{

"lien_id": "LNK456",

"lien_holder_key": "0x123GHI...",

"amount_usd": 210450.75,

"type": "MORTGAGE",

"recorded_timestamp": "2018-05-20T10:00:00Z"

}

],

"covenants_restrictions_hash": "b3d5b...",

"zoning_classification": "R-1",

"tax_assessment_usd": 350000,

"transaction_history": [

"0xTXHASH...",

"0xTXHASH...",

"0xTXHASH..."

]

}

This structure forces clarity. Ambiguities that hide in long legal paragraphs are stripped away. Is there a lien? It’s in the `liens` array. Who owns it? The `owner_public_key` says so. The entire history is a verifiable chain of transaction hashes. The need for a human to read decades of deeds and interpret handwritten notes is engineered out of the system.

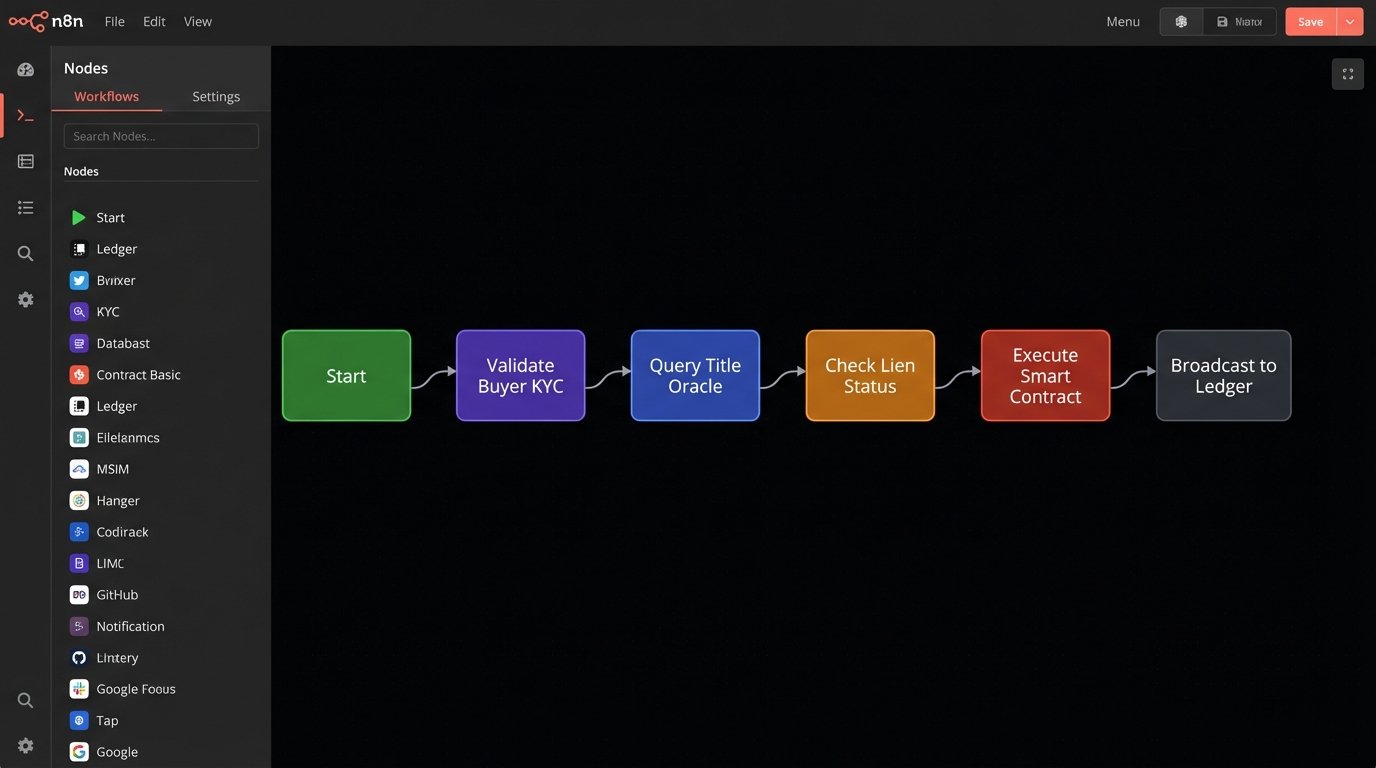

Replacing Human Middleware with Smart Contracts

With a tokenized title, the closing process becomes a state machine managed by a smart contract. This isn’t artificial intelligence. It’s a simple, deterministic script that executes predefined logic when specific conditions are met. It is the escrow agent, the closing attorney, and the settlement officer, all converted into immutable code.

The contract holds all assets in escrow digitally: the buyer’s funds (as stablecoins or tokenized dollars) and the seller’s property token. It then monitors for the fulfillment of all contingencies, which are no longer lines in a PDF but functions in the contract itself.

Think about the inspection contingency. Today, this involves emailing a report, negotiating repairs via phone, and signing an addendum. In an automated system, the process is reduced to an external data call. An oracle, a trusted data feed, pushes the inspection result to the smart contract.

A Logic Check for Contingency Fulfillment

The smart contract’s logic is brutally simple. It operates as a series of pass/fail gates. Does the inspection report meet the contract’s criteria? Does the appraisal value from the lender’s API meet or exceed the purchase price? Has the buyer’s funding been confirmed on-chain?

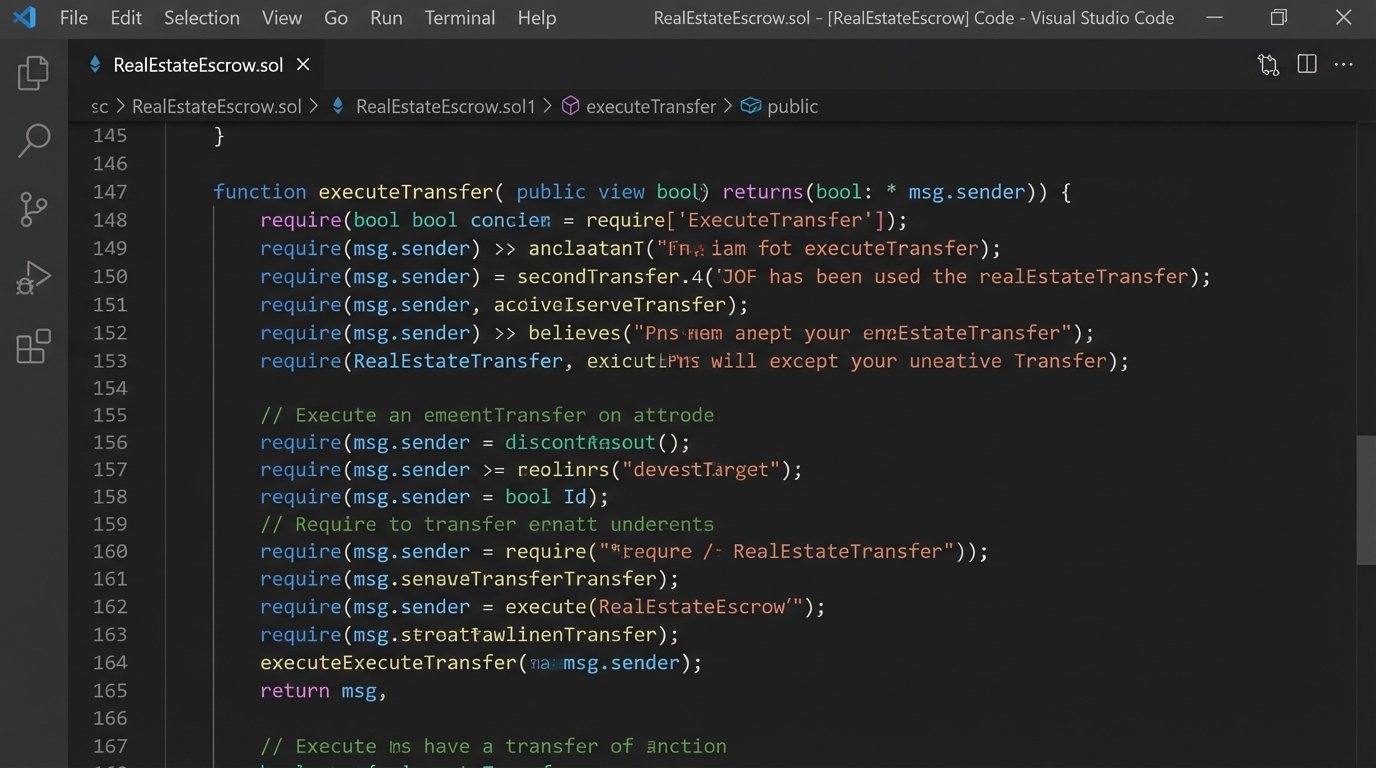

Here’s a pseudocode sketch of what that logic might look like inside the contract:

function executeTransfer(propertyTokenId, buyerKey) {

// Logic-check preconditions

require(msg.sender == buyerKey, "Only buyer can trigger.");

require(contractState == "CONTINGENCIES_PENDING", "Invalid state.");

// Check data from external oracles

bool inspectionPassed = checkInspectionOracle(propertyTokenId);

bool financingApproved = checkLenderOracle(buyerKey);

bool titleIsClear = checkTitleOracle(propertyTokenId);

require(inspectionPassed, "Inspection failed.");

require(financingApproved, "Financing denied.");

require(titleIsClear, "Title is not clear.");

// All checks passed. Execute the state change.

contractState = "SETTLED";

releaseFundsTo(sellerKey);

transferTokenTo(buyerKey, propertyTokenId);

logTransaction(propertyTokenId, buyerKey, sellerKey);

}

When `executeTransfer()` is called and all `require` statements pass, the swap happens instantly and atomically. The funds move to the seller’s wallet, and the property token moves to the buyer’s wallet. There is no settlement gap. There is no “funding condition” delay. The transaction and its recording are one and the same.

The Messy Reality: The Data Ingestion Problem

This vision of clean, programmatic execution hinges on one massive, ugly problem: getting reliable data into the system. The smart contract is deterministic; it cannot function with ambiguous or dirty data. Building the API bridges to the outside world is where this entire concept faces its trial by fire. This is the equivalent of shoving a firehose of unstructured data through the needle-eye of a strict data schema.

Municipal databases are a nightmare. Some counties offer REST APIs, but they are often unreliable, poorly documented, and subject to absurd rate limits. Others still require scraping HTML tables from websites running on ColdFusion. Some require you to submit a physical form. Bridging this gap requires a massive investment in data engineering to normalize, clean, and validate information before it can ever touch a smart contract oracle.

Lenders, inspectors, and insurance providers are no better. Each has their own proprietary data format. You end up building a brittle network of bespoke parsers and adapters, each one a potential point of failure. A single change in a lender’s API response can break a transaction flow. This is not a trivial engineering challenge; it is the central obstacle.

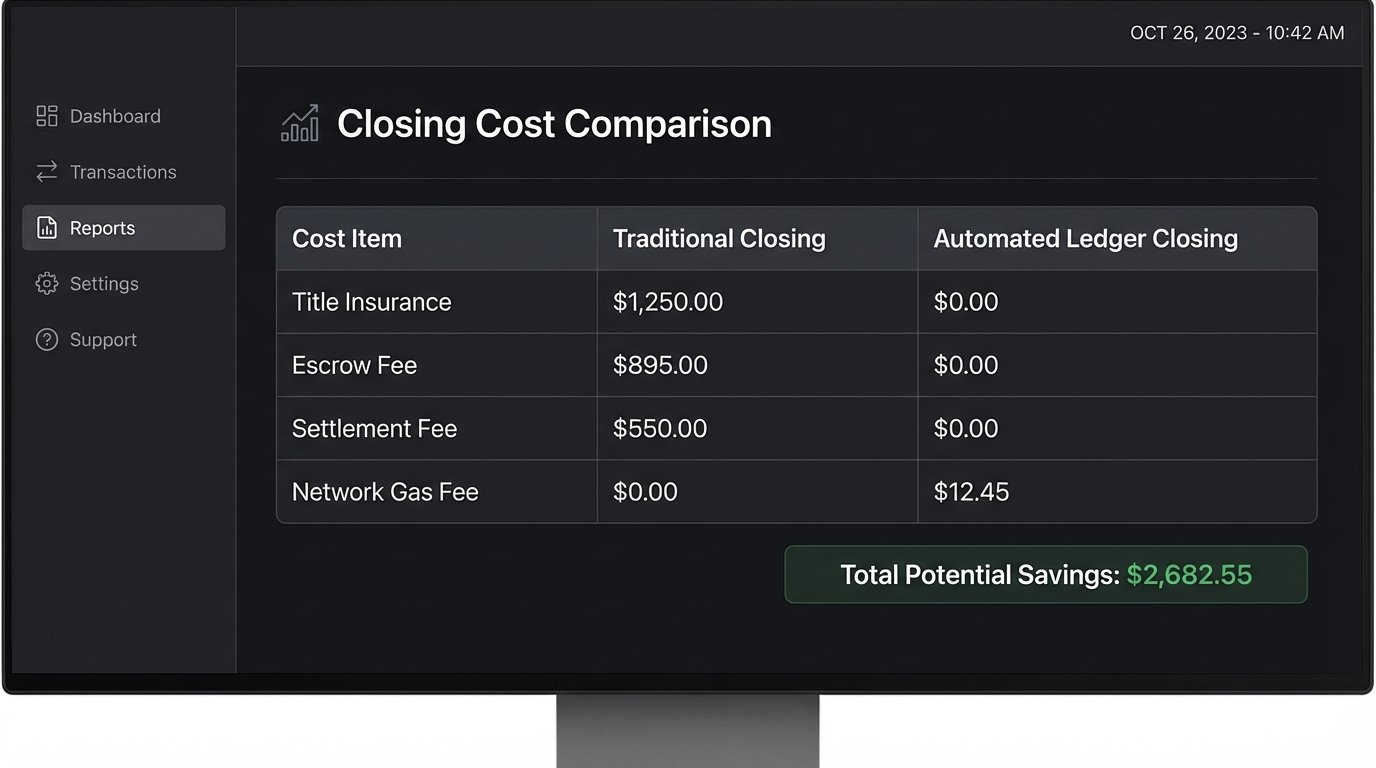

Deconstructing the Fee Stack

A fully automated system doesn’t just change the workflow; it annihilates the existing fee structure. The value propositions of several key players are rendered obsolete by the architecture.

- Title Insurance: Its entire purpose is to insure against human error in the title search process. An immutable ledger with a verifiable cryptographic history of ownership requires no such insurance. The risk of a defect in the chain of title is mathematically eliminated. This removes a significant closing cost.

- Escrow Fees: The smart contract is the escrow agent. It holds assets based on unbreakable coded instructions. There is no need for a trusted human intermediary or the associated fee.

- Settlement and Closing Fees: The settlement is the atomic transaction executed by the smart contract. There is no closing table, no signing ceremony, and no need for an agent to coordinate the disbursement of funds.

- Recording Fees: The fee to record the transaction is the network’s gas fee, which is transparent and typically far lower than the fees charged by a county recorder to manually stamp and scan a document.

The result is a transaction that is not only faster but orders of magnitude cheaper. The human latency and risk mitigation products that bloat a closing statement are systematically stripped out by the code.

The True Barriers Are Human, Not Technical

The technology to build this system exists today. We have distributed ledgers, mature smart contract platforms, and the tools to build secure oracles. The code is the easy part. The real roadblocks are the legal and regulatory frameworks built around the paper-based process, and the entrenched industries that profit from its inefficiency.

County recorders will not willingly cede their authority to a distributed network. State legislatures will need to pass laws that recognize a cryptographic transfer of a token as a legally binding property conveyance. The title insurance industry, a multi-billion dollar behemoth, will lobby hard to protect its state-mandated existence. These are not engineering problems. They are political battles.

Furthermore, there is immense inertia. The entire ecosystem of real estate agents, lenders, and lawyers is trained on the current system. Retooling an entire profession is a generational challenge. The initial implementations of such a system will likely be confined to specific jurisdictions or asset classes willing to experiment, running in parallel with the old system for years.

Building this future is not about finding a clever algorithm. It’s about having the political will and capital to hammer a new set of rails into a landscape where everyone is perfectly happy with the horse and buggy.