Stop Talking About Blockchain Revolutionizing Real Estate. It Won’t.

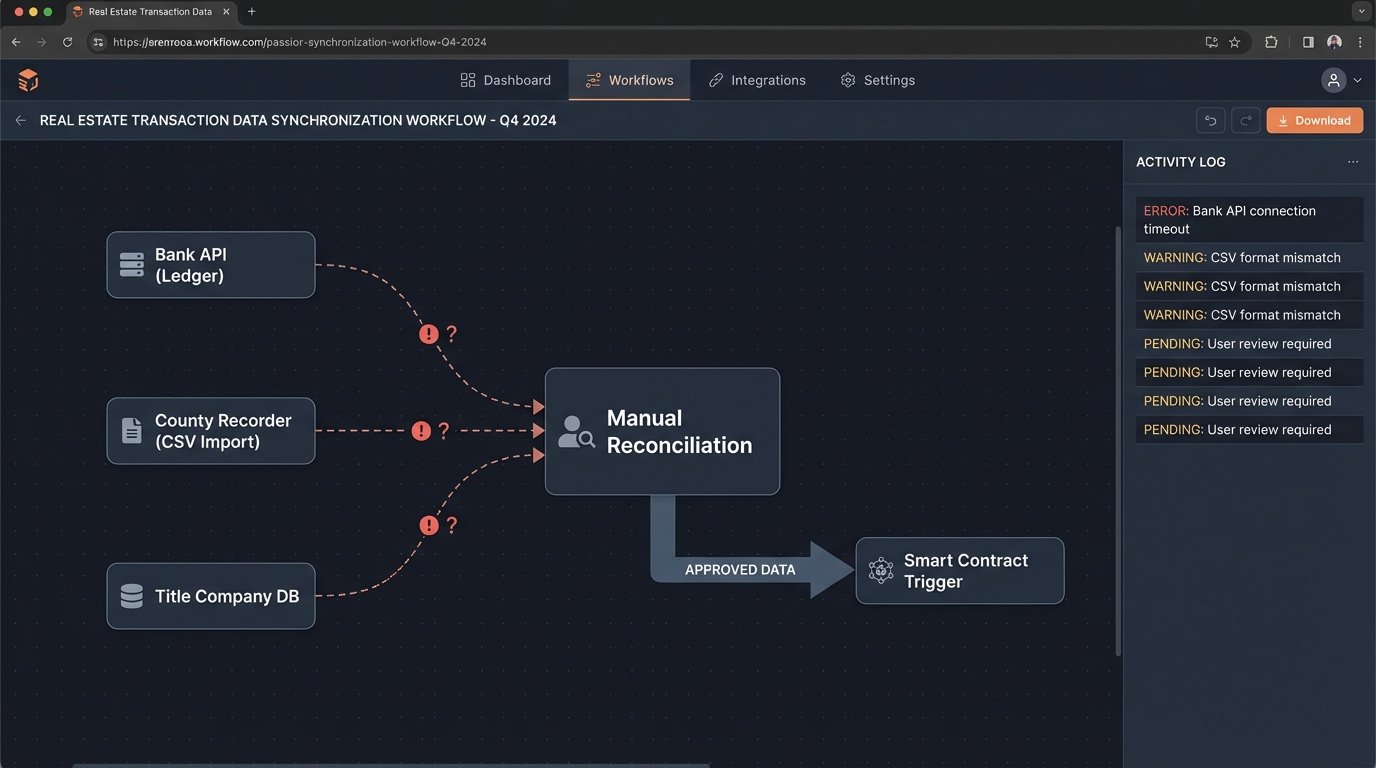

The core of every real estate transaction is a series of database updates. The bank’s ledger changes. The county recorder’s database gets a new entry. The title company updates its records. These databases don’t talk to each other, are frequently out of sync, and are protected by layers of manual verification that exist only because nobody trusts anyone else’s data. This multi-party reconciliation problem is the source of the friction, the cost, and the five-week closing cycles we accept as normal.

We are told that blockchain, with its shared, immutable ledger, is the fix. The theory is clean. A single, append-only source of truth that all parties in a transaction, the buyer, seller, lender, and county clerk, can read from and write to. In this perfect world, a property title is a non-fungible token, escrow is a smart contract, and the closing is an atomic transaction that settles in seconds, not weeks.

This narrative is simple, compelling, and mostly wrong. It ignores the messy reality of interfacing a cryptographically secure state machine with a world of paper deeds, underfunded municipal IT departments, and banking regulations written in the 1970s. The fantasy of a fully on-chain real estate transaction falls apart the moment it touches the physical world.

The real value is far less glamorous and much harder to implement.

The Smart Contract Paradox

A smart contract is just code. It’s a script stored on a blockchain that executes when predetermined conditions are met. For a property sale, the logic might look like this: IF the buyer’s funds are confirmed, AND the title is clear, AND the inspection is approved, THEN transfer the digital title asset to the buyer’s wallet and release the funds to the seller’s wallet. This code automates the escrow agent out of a job.

The problem is the conditions. A smart contract can cryptographically verify on-chain conditions, like the presence of funds in a wallet. It cannot, however, verify off-chain events. It has no way to know if a termite inspection passed or if the seller fixed the leaking roof as promised. This is the infamous “oracle problem”. To get this external data onto the blockchain, you need a trusted entity, an oracle, to report the real-world outcome.

Suddenly, we’ve reintroduced a trusted third party. We’ve just swapped a licensed escrow agent for a data feed API. If that oracle’s API is compromised or simply reports incorrect data, the smart contract will execute flawlessly based on faulty information. We’ve automated the failure, making it happen faster and with cryptographic finality. This isn’t an improvement. It’s just a new kind of risk.

You haven’t eliminated trust. You’ve just moved it to a different box on the flowchart.

The On-Ramp Is a Dirt Road

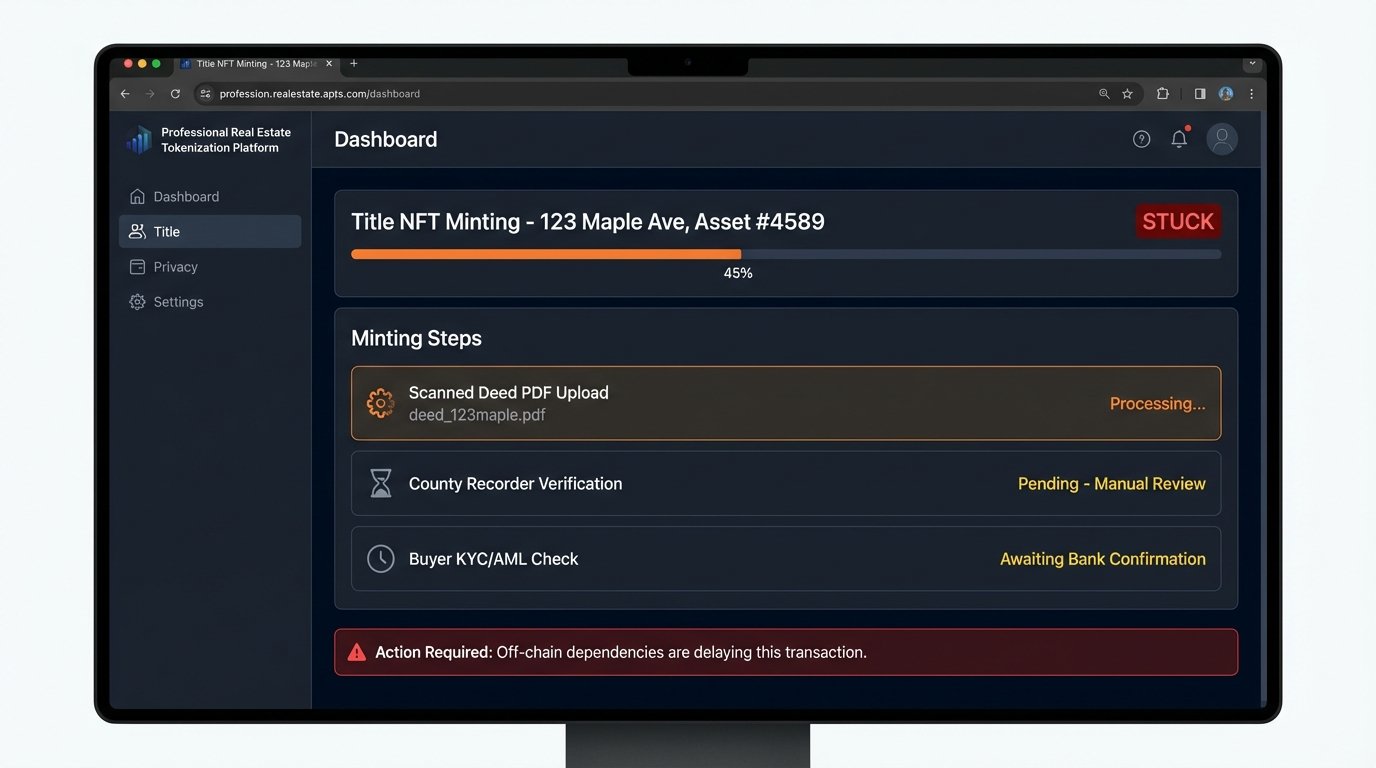

Getting assets onto a blockchain is the single greatest technical and procedural hurdle. Before you can execute a smart contract for a home sale, two things must happen. First, the property title must be tokenized into a unique digital asset on the chain. Second, the buyer’s fiat currency, their US dollars, must be represented on-chain, typically as a stablecoin.

Tokenizing a title is not a simple database entry. It requires a legal framework that recognizes a digital token as a bearer instrument for real property ownership. No county recorder’s office in the United States is currently equipped to handle this. They record PDF scans of paper documents. Their entire system is built around ink signatures and notary stamps. Bridging this gap requires rewriting state and federal property laws.

The currency on-ramp is equally problematic. While stablecoins like USDC are well-established, moving a few hundred thousand dollars for a down payment triggers all manner of AML and KYC checks. The process involves legacy bank wires, ACH transfers, and verification delays. The dream of an instantaneous, peer-to-peer transaction is bottlenecked by the very banking infrastructure it aims to bypass. It feels like trying to shove a firehose of data through a rusty garden spigot.

You can’t claim to be a frictionless system when your entry and exit points are all friction.

Where It Might Actually Work: A Hybrid Approach

A pure, end-to-end on-chain real estate transaction is a distraction. The pragmatic application of this technology is a hybrid model. We use the blockchain not as the entire engine, but as a specialized component, a gear for a very specific job: creating an immutable audit trail. Forget running the whole transaction on-chain. Focus on using a distributed ledger to solve the nastiest data integrity problems.

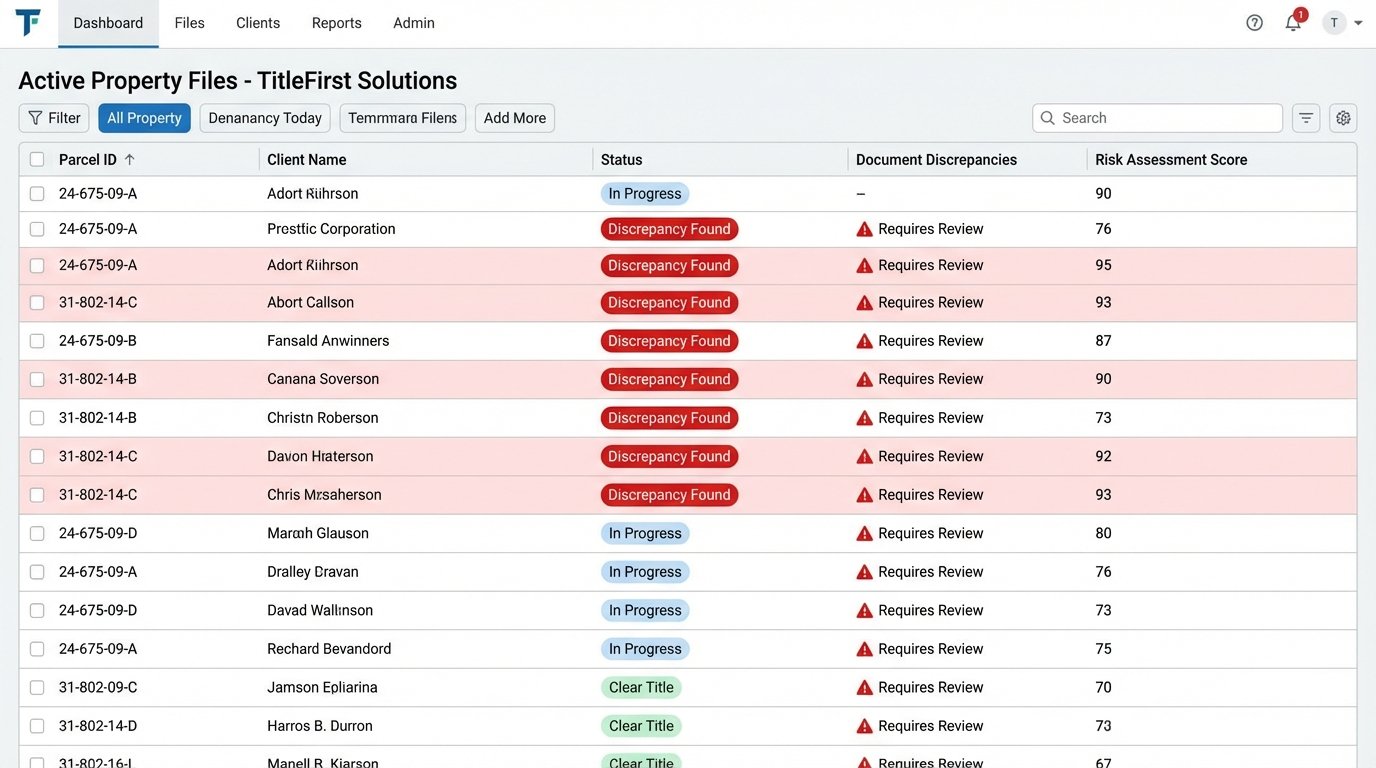

The most immediate and valuable use case is the title chain of custody. Instead of a title search involving weeks of digging through fragmented, error-prone county records, imagine a permissioned ledger. Every event in the property’s history, the original plat, every sale, every lien filed, every easement granted, is a transaction on the ledger. Each entry is cryptographically signed and linked to the one before it, creating an unbreakable chain of provenance.

This doesn’t replace the county recorder. It augments it. The legal documents are still filed, but a hash of each document, along with key metadata, is committed to the chain. Title insurance, an industry that exists solely to underwrite the risk of poor record-keeping, would see its core business model gutted. This is not about disruption. It’s about building a better, more verifiable logging system.

A basic data structure for this on-chain record might look something like this in Solidity.

pragma solidity ^0.8.0;

contract PropertyTitle {

struct TitleRecord {

uint256 blockTimestamp;

address from;

address to;

string documentHash; // IPFS hash of the scanned legal document

string eventType; // e.g., "SALE", "LIEN", "EASEMENT"

}

mapping(string => TitleRecord[]) public titleHistory; // APN to history array

mapping(string => address) public currentOwner; // APN to current owner

function transferTitle(string memory parcelNumber, address _from, address _to, string memory _docHash) internal {

// Logic check: only current owner can initiate transfer

require(currentOwner[parcelNumber] == _from, "Sender is not the current owner.");

TitleRecord memory newRecord = TitleRecord({

blockTimestamp: block.timestamp,

from: _from,

to: _to,

documentHash: _docHash,

eventType: "SALE"

});

titleHistory[parcelNumber].push(newRecord);

currentOwner[parcelNumber] = _to;

}

}

This code doesn’t execute the entire sale. It just provides a bulletproof mechanism for recording the transfer of ownership after the fact. The real-world legal and financial processes still happen off-chain, but the result is anchored to an immutable record. This is a realistic, achievable goal that delivers immediate value by reducing ambiguity and the cost of verification.

The Real Obstacles Are Not Technical

We can engineer our way around the oracle problem with sophisticated consensus mechanisms. We can build better fiat on-ramps. We can design more efficient private ledgers that handle transaction throughput. The technology is the easy part. The true roadblocks are data standardization and the entrenched interests that profit from the current mess.

There is no standard data format for a property deed in the United States. Each of the 3,000-plus counties has its own forms, its own fields, its own way of recording information. Before you can automate anything, you must first structure the data. This requires a massive, coordinated effort to create a universal schema for property records. This is a grueling, unglamorous data engineering project, not a sexy blockchain one.

Then you have the ecosystem of incumbents. Title insurers, escrow agents, real estate lawyers, and mortgage brokers all take a slice of the transaction. Their business models are predicated on complexity and information asymmetry. A transparent, efficient, automated system is a direct threat to their revenue. They have entire lobbying arms dedicated to preserving this status quo.

They are not going to endorse a system that makes them obsolete.

A Forced Evolution, Not a Revolution

Blockchain’s impact on real estate will be slow, painful, and indirect. It will not be a sudden shift to a fully tokenized world. Instead, the principles of distributed ledger technology will force a long-overdue conversation about data standards and process simplification. The threat of being made irrelevant by a more efficient model will compel lenders, title companies, and government agencies to finally modernize their infrastructure.

The win isn’t putting every deed on a public chain. The win is forcing the creation of a standardized API for every county recorder’s office so a title search can be an automated query instead of a manual process. The win is developing a universal data format for mortgages so they can be processed and underwritten with minimal human intervention.

If this happens, the underlying technology, whether it’s a true blockchain, a centralized database with better APIs, or some other distributed ledger tech, is almost irrelevant. The real work is in the plumbing. It’s about agreeing on the size and shape of the pipes. The current obsession with the blockchain brand name misses this point entirely. We’re arguing about the faucet design while the foundation is rotten.